เคทีซีกำไรสุทธิ 9 เดือน 4,011 ล้านบาท ปรับกลยุทธ์ฝ่าวิกฤติเศรษฐกิจ

เคทีซีกำไรสุทธิ 9 เดือน 4,011 ล้านบาท

ปรับกลยุทธ์ฝ่าวิกฤติเศรษฐกิจ เดินหน้าโมเดลธุรกิจใหม่ คุมต้นทุนค่าใช้จ่ายการเงิน

เคทีซีแจ้งผลประกอบการ 9 เดือนแรก ภายใต้มาตรฐานใหม่ TFRS9 กำไรสุทธิ 4,011 ล้านบาท ฐานสมาชิกรวม 3.5 ล้านบัญชี หนี้ที่ไม่ก่อให้เกิดรายได้ (NPL) ลดลง นำทัพเดินหน้าฝ่าวิกฤติเศรษฐกิจและมาตรการต่างๆ ปรับกระบวนการทำงานครั้งใหญ่ทั้งองคาพยพให้มีประสิทธิภาพ ลดต้นทุนการดำเนินงานและคุมค่าใช้จ่ายทางการเงิน อัดยาแรงรุกโมเดลธุรกิจใหม่ “พี่เบิ้ม” ควบศึกษาแผนงานระบบการชำระเงิน หวังเสริมธุรกิจหลัก สร้างโอกาสให้บริษัทเติบโตยั่งยืนระยะยาว

นายระเฑียร ศรีมงคล ประธานเจ้าหน้าที่บริหาร “เคทีซี” หรือ บริษัท บัตรกรุงไทย จำกัด (มหาชน) กล่าวว่า “สถานการณ์ทางเศรษฐกิจในไตรมาสที่ 3 เริ่มส่งสัญญาณดีขึ้น จากการผ่อนคลายมาตรการต่างๆ ลง เราเริ่มเห็นความร่วมมือของผู้ประกอบการที่พร้อมจะช่วยกันฟื้นฟูประเทศในรูปแบบต่างๆ เพื่อช่วยกันให้ประเทศไทยไปต่อ สร้างโอกาสสนับสนุนให้คนไทยสร้างอาชีพและรายได้ ทำให้สัญญาณความเชื่อมั่นของผู้บริโภคและการใช้จ่ายภาคประชาชนเป็นไปในทางที่ดีขึ้น และเมื่อมองกลับมาที่เคทีซีในช่วง 9 เดือนที่ผ่านมา ถือว่าปริมาณการใช้จ่ายผ่านบัตรเครดิตเริ่มปรับตัวดีขึ้นเป็นลำดับ พอร์ตลูกหนี้ขยายตัวเพิ่มขึ้น 5.9% ควบคุมค่าใช้จ่ายทางการเงินได้ดี และมีรายได้หนี้สูญได้รับคืนอยู่ในระดับที่น่าพอใจ”

“อย่างไรก็ตาม บริษัทฯ ยังได้รับผลกระทบในการสร้างรายได้ เนื่องจากข้อจำกัดเรื่องเพดานอัตราดอกเบี้ยของ 2 ธุรกิจหลักที่ลดลง คือ ธุรกิจบัตรเครดิตลดลงที่ 2% และสินเชื่อบุคคลลดลงที่ 3% อีกทั้งการให้ความช่วยเหลือด้านสินเชื่อสำหรับลูกหนี้ที่ได้รับผลกระทบจากโควิด-19 ตามมาตรการของกระทรวงการคลังและธนาคารแห่งประเทศไทย โดยมีกลุ่มลูกหนี้ที่สมัครเข้าร่วมปรับโครงสร้างหนี้กับเคทีซีประมาณ 7,800 ราย คิดเป็นมูลหนี้รวม 600 ล้านบาท (ข้อมูล ณ วันที่ 30 กันยายน 2563) ทำให้บริษัทฯ ต้องเร่งปรับกลยุทธ์สร้างโมเดลธุรกิจใหม่เพื่อเพิ่มโอกาสในการทำรายได้ รวมทั้งปรับกระบวนการทำงานทั่วทั้งองค์กรให้มีประสิทธิภาพมากขึ้น เพื่อลดต้นทุนการดำเนินงาน รวมทั้ง ตัดหนี้สูญเพื่อให้พอร์ตลูกหนี้สะท้อนภาพความเป็นจริงมากขึ้น

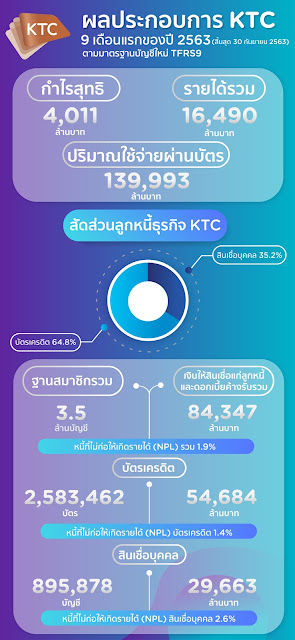

ณ วันที่ 30 กันยายน 2563 ภายใต้มาตรฐานบัญชีใหม่ TFRS9 เคทีซีมีกำไรสุทธิ 9 เดือน 4,011 ล้านบาท และกำไรสุทธิไตรมาส 3 เท่ากับ 1,221 ล้านบาท เงินให้สินเชื่อแก่ลูกหนี้และดอกเบี้ยค้างรับรวม เท่ากับ 84,347 ล้านบาท (ขยายตัว 5.9%) ฐานสมาชิกรวม 3.5 ล้านบัญชี แบ่งเป็นบัตรเครดิต 2,583,462 บัตร (ขยายตัว 5%)เงินให้สินเชื่อแก่ลูกหนี้บัตรเครดิตและดอกเบี้ยค้างรับรวม54,684 ล้านบาท (ขยายตัว 6.9%) อัตราเติบโตของปริมาณ ใช้จ่ายผ่านบัตรเครดิต 9 เดือน อยู่ที่ -8.3% หรือมีมูลค่ารวมทั้งสิ้น 139,993 ล้านบาท NPL รวม ลดเหลือ 1.9% NPL บัตรเครดิตอยู่ที่ 1.4% สินเชื่อบุคคล (รวมสินเชื่อธนวัฏและสินเชื่อเจ้าของกิจการ)895,878 บัญชี (ลดลง 8% จากการปิดบัญชีที่ไม่เคลื่อนไหวในช่วงที่ผ่านมา) เงินให้สินเชื่อแก่ลูกหนี้สินเชื่อบุคคลและดอกเบี้ยค้างรับรวม 29,663 ล้านบาท (เติบโต 5.1%) NPL ของสินเชื่อบุคคลอยู่ที่ 2.6%

ในช่วง 9 เดือนที่ผ่านมา เคทีซีมีรายได้ดอกเบี้ยรวม (รวมค่าธรรมเนียมในการใช้วงเงิน) ไตรมาส 3 และ 9 เดือนของปี 2563 เท่ากับ 3,498 ล้านบาท เพิ่มขึ้น 2.1% เมื่อเทียบกับช่วงเดียวกันของปีก่อน และ 10,745 ล้านบาท เพิ่มขึ้น 7.3% ตามลำดับ ขณะที่รายได้ค่าธรรมเนียม (ไม่รวมค่าธรรมเนียมการใช้วงเงิน) มีมูลค่าเท่ากับ 1,093 ล้านบาท ลดลงที่ -10.3% และ 3,245 ล้านบาท ลดลงที่ -11.6% ตามลำดับ ในขณะที่ค่าใช้จ่ายดำเนินงานต่อรายได้รวม (Cost to Income Ratio) เท่ากับ 31.7% ลดลงจาก 34.0% ณ ช่วงเวลาเดียวกันของปีก่อนหน้า เนื่องจากบริษัทฯ เน้นทำการตลาดออนไลน์มากขึ้น และลดการจัดกิจกรรมการตลาดทั้งในการจัดหาบัตรใหม่และการส่งเสริมการใช้จ่ายผ่านบัตร

สำหรับรายได้รวม 9 เดือนปี 2563 เท่ากับ 16,490 ล้านบาท ลดลงเล็กน้อยที่ -1% เมื่อเทียบกับช่วงเดียวกันของปีก่อน โดยมาจากรายได้ดอกเบี้ยลูกหนี้บัตรเครดิตและลูกหนี้สินเชื่อบุคคลที่เพิ่ม 9% และ 6% ตามลำดับ เป็นอัตราเพิ่มที่ชะลอตัวลงจากผลกระทบสืบเนื่องจากโควิด-19 และการลดเพดานอัตราดอกเบี้ยของธนาคารแห่งประเทศไทย สำหรับค่าใช้จ่ายรวมเท่ากับ 11,476 ล้านบาท แบ่งเป็นค่าใช้จ่ายบริหารงาน 5,223 ล้านบาท ผลขาดทุนด้านเครดิตที่คาดว่าจะเกิดขึ้น (หนี้สูญและหนี้สงสัยจะสูญ) 5,095 ล้านบาท และต้นทุนทางการเงิน 1,159 ล้านบาท ตามลำดับ ค่าใช้จ่ายในการบริหารลดลง 8% จากรายการทางการค้าและกิจกรรมการตลาดที่ลดลง ผลขาดทุนด้านเครดิตที่คาดว่าจะเกิดขึ้น (หนี้สูญและหนี้สงสัยจะสูญ) มีมูลค่าทั้งสิ้น 5,095 ล้านบาท เพิ่มขึ้น 11% เมื่อเทียบกับปีก่อนหน้า แบ่งเป็นหนี้สูญ 3,734 ล้านบาท และหนี้สงสัยจะสูญ 1,361 ล้านบาท

นายระเฑียรกล่าวเพิ่มเติมว่า “จากวิกฤตโรคระบาดที่รวดเร็วรุนแรงทั่วโลกและยังไม่มีจุดสิ้นสุด ประกอบกับกฎเกณฑ์ของหน่วยงานกำกับดูแลที่ปรับเปลี่ยนต่อเนื่อง ทำให้เคทีซีต้องปรับตัวครั้งใหญ่ในลักษณะของการทำลายอย่างสร้างสรรค์หรือที่เรียกว่า Creative Disruption โดยพิจารณาสร้างโมเดลธุรกิจใหม่ขึ้นมาสนับสนุนธุรกิจหลักเดิม ด้วยการศึกษาและทดลองตลาดผลิตภัณฑ์ทางการเงินใหม่ๆ หลายรูปแบบที่ต่างจากเดิม ไม่ว่าจะเป็น “พิโก ไฟแนนซ์” สินเชื่อรายย่อยระดับจังหวัดสำหรับบุคคลธรรมดากู้ยืมไปใช้จ่ายส่วนตัว หรือ “นาโน ไฟแนนซ์” สินเชื่อรายย่อยเพื่อการประกอบอาชีพ และสินเชื่อที่มีทะเบียนรถเป็นประกัน และในที่สุดได้ตัดสินใจเปิดสินเชื่อใหม่หลากรูปแบบขึ้นเมื่อเร็วๆ นี้ ภายใต้แบรนด์ “เคทีซี พี่เบิ้ม” ในรูปแบบของสินเชื่อที่มีหลักประกัน ครอบคลุมทั้งสินเชื่อทะเบียนรถยนต์และสินเชื่อทะเบียนรถจักรยานยนต์ ซึ่งเป็นธุรกิจที่มีความเสี่ยงต่ำ ให้ผลตอบแทนที่รวดเร็วและสอดคล้องกับ สภาะเศรษฐกิจปัจจุบัน โดยคาดว่าสินเชื่อภายใต้แบรนด์ “เคทีซี พี่เบิ้ม” จะเป็นหนึ่งในฐานการทำธุรกิจใหม่ของเคทีซี นอกจากนี้ บริษัทฯ ยังอยู่ในระหว่างการศึกษาข้อมูลและวิธีดำเนินโครงการเกี่ยวกับระบบการชำระเงิน (Payment System) ซึ่งคาดว่าจะเป็นธุรกิจใหม่ที่จะมาเสริมธุรกิจหลัก และสร้างโอกาสให้บริษัทเติบโตได้อย่างยั่งยืนในระยะยาว

KTC announces 4.011 million in 9M profits with strategy adjustments to combat the economic crisis and moves forward with a new business model

to control financial costs.

KTC reports its 9M/2020 business operations under the new TFRS9 standard, announcing 4,011 million in profits, 3.5 million in total member accounts, and a decrease in NPL. The company is ready at full force to combat the economic crisis and other policies with major adjustments in business operations, including efficient work processing, operating cost reductions, and financial cost control. The company moves forward with the all-new “P BERM” business model along with studies on the payment system plan to strengthen the core business and generate long-term growth opportunity for the company.

Mr. Rathian Srimongkol, President & Chief Executive Officer, “KTC” or Krungthai Card Public Company Limited, states, “The economic situation in Q3 has shown signs of improvement due to easing measures. We began to see collaboration from entrepreneurs who are ready to revitalize the country in a variety of ways for Thailand to move forward, and create opportunities to support Thais to find employment and income, which caused a positive growth in terms of consumer confidence and public spending. Examining KTC in the last 9 months in retrospect, credit card spending had begun to improve accordingly; total the receivable portfolio expanded by 5.9 percent with good control of financial costs and a satisfactory level of bad debt.”

“Despite this, the company has been affected in regards to income generation due to limitations stemming from lower interest rate ceilings for the two main businesses. This includes a 2 percent drop for the credit card business and 3 percent for personal loans, as well as KTC's credit support for debtors affected by COVID-19 in accordance with The Ministry of Finance’s and The Bank of Thailand’s measures. There were debtor groups consisting of an approximate of 7,800 individuals who applied to join KTC's debt restructuring campaign which amounted in a total debt of 600 million Baht (information as of September 30, 2020). These factors prompted the company had also improved its entire work process to be more efficient in order to lower its operating cost, as well as writing off bad debts to truly reflect the reality of receivable portfolio.”

“As of September 30, 2020, under the new TFRS9 standard, KTC has a 9 month net profit of 4,011 million baht and 1,221 million baht for Q3. Total loan to customers and accrued interest receivables totalled 84,347 million baht (5.9 percent growth) and total member of 3.5 million accounts,comprising of 2,583,462 credit cards (5 percent increase), Total loans to credit card debtors and accrued interest receivables of 54,684 million baht (6.9 percent increase). The rate of credit card spending in the past 9 months is at -8.3 percent or a total of 139,993 million Baht, Overall NPL dropped to 1.9 percent and the NPL for credit cards totalled 1.4 percent. Personal loans accounts (including circle loans and self-employed loans) numbered 895,878 accounts (8 percent decrease due to account inactivity). Loans to personal loans customers and total accrued interest receivables amounted to 29,663 million baht (5.1 percent growth), and NPL for the personal loans business totalled 2.6 percent.”

“In the past 9 months, the company accumulated a net interest income (including credit usage fees) for Q3 and the first 9 months of 2020 at 3,498 million baht, a 2.1 percent increase compared to the same period last year, and 10,745 million baht, a 7.3 percent increase respectively. Meanwhile, income from fees (excluding credit usage fees) totalled 1,093 million baht, a -10.3% decrease, and 3,245 million baht, a -11.6% decrease respectively. At the same time, the cost to income was 31.7 percent, a drop 34.0 percent from the same period of last year owing to the fact that the company had focused more of its efforts on online marketing and reduced marketing activities for both new card acquisitions and card spending promotions.”

“KTC's total income for 9 months of 2020 amounted to 16,490 million baht, a slight -1 percent decrease compared to the same period last year. This is due to income gained from interest from credit card and personal loans receivables, which increased by 9 and 6 percent respectively. These rates are slower increases as a result of the effects of COVID-19 and The Bank of Thailand's reductions in the interest rate ceiling. Overall expenses totalled 11,476 million baht, from 5,223 million baht in operation fees, 5,095 million baht in expected credit loss (bad debt and doubtful accounts) and 1,159 million baht in financial costs respectively. Administrative expenses were reduced by 8 percent due to the decrease in commercial transactions and marketing activities. Expected credit loss (bad debt and doubtful accounts) totalled 5,095 million baht, an 11 percent increase compared to the same period last year, which can be broken down into 3,734 million baht of bad debt and 1,361 million baht of doubtful accounts.”

Mr. Rathian adds, “As a consequence of a global pandemic that spread rapidly and still have no sign of ending, coupled with continuously changing regulations of regulators, KTC had to make major adjustments in the form of creative disruption by considering creating a new business model to support the old core business. This was achieved by studying and testing the market of new financial products in a variety of new ways whether it be “Pico Finance,” provincial-level micro-loans for personal expenses, or “Nano Finance,” micro loans for occupation and loans with car license plates as collateral. Recently, KTC finally decided to launch a new loan in a different style under the “KTC P BERM” brand in the form of collateralized loans covering both car and motorcycle registration loans. This type of loan is considered low-risk and provides quick returns, consistent with the current economic situation. It is expected that loans under the “KTC P BERM” brand will become one of the new bases for KTC's business. Moreover, the Firm is in the process of studying information and project implementation methods on payment systems, and it is expected to become a new business that will play a role in complementing the core business and generate long term and consistent growth opportunity for the company.”